The world has not yet begun to deleverage its crisis-linked borrowing, a recent report by the International Centre for Monetary and Banking Studies (ICMBS) found. Despite currently prevailing popular opinion that the global economy is deleveraging, the world is in fact not reducing the burden of its debts, according to the organization’s research; in fact, public sector debt in rich countries and private debt in emerging markets–notably China–have not stopped rising, and this may cause a new economic crisis.

“Contrary to widely held beliefs, the world has not yet begun to delever and the global debt to GDP ratio is still growing, breaking new highs,” said the report.

The document, the 16th annual Geneva Report, titled “Deleveraging? What deleveraging?,” was commissioned by the ICMBS and written by a panel of senior economists, and was published on the Centre for Economic Policy Research website.

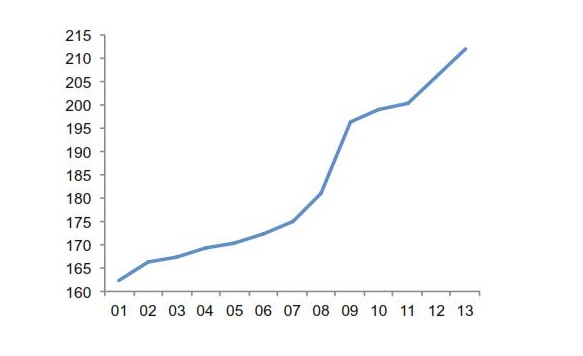

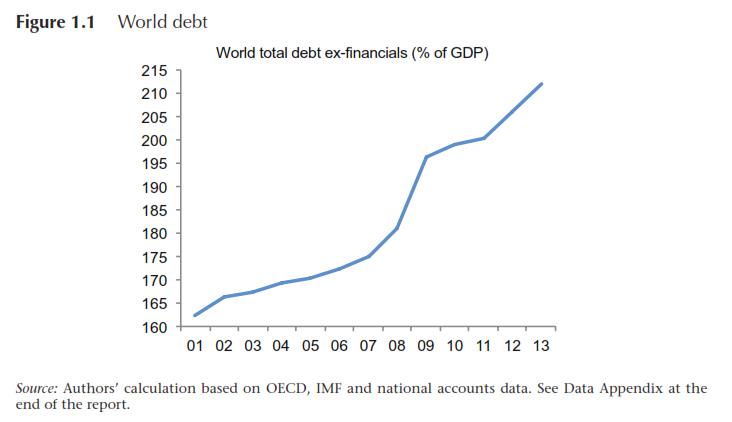

The total burden of world debt–private and public–has reached 215 percent of national income. For perspective, the whole world would need to consume nothing while continuing current levels of production for two years in order to pay back the world debt.

That burden was only 160 percent of national income in 2001, and under 200 percent in 2009.

The report notes that debt growth was primarily in the private sector of the developed world before the financial crisis. After the crisis, Western governments accepted a lot of debt, which reduced the burden on the private sector.

Meanwhile, developing countries like China increased debt when they saw that Western economies would not be able to sustain the rapid growth, the report found.

The report characterized the combination of record debt and slowing growth as a “poisonous combination” that pointed toward further economic crisis.

The report stressed economies with high debts and persistently slow growth–such as the eurozone periphery in southern Europe and China–as economies that were most concerning.

An author of the report, Luigi Buttiglione, compared China to past miracle economies. “Over my career I have seen many so-called miracle economies – Italy in the 1960s, Japan, the Asian tigers, Ireland, Spain and now perhaps China–and they all ended after a build-up of debt.”

The report suggested a possible model that may explain the current existence of debt bubbles: innovation tends to increase productivity–therefore growth. Market participants become more optimistic and credit is easier to obtain, leading to more loans. Loans are often tied to a project and show up as more growth, which further nurtures optimism and increases loans, even if the underlying productivity gains have run their course.

The authors of the report concluded that in order to avoid another crash, interest rates across the world will have to stay low for a “very, very long” time to enable households, companies and governments to alleviate their debts.

The report was published a week before the International Monetary Fund’s annual meeting in Washington and concerns that the US Federal Reserve will raise interest rates within the year.

By Andrew Stern